Synopsis

1. Like all real asset classes, the Office is also seeing significant short term impacts from the COVID-19 Pandemic and the forced proliferation of Work From Home.

2. There are some benefits in the WFH paradigm but there are many issues as well as companies and employees are increasingly coming to realize.

3. The office market is staging a strong recovery in terms of leasing and transactions around the world.

4. The Office continues to hold many advantages as a primary place of work due to its ability to boost productivity, innovation, collaboration and socialization as well as to mitigate many of the issues related to remote work, such as burn out and other psychological issues.

5. The Office will have to adapt to cater to new, often hybrid models of work, to promote the wellness of its occupants and to provide them with a high-quality experience. This creates greater relevance to the Co-Working paradigm and to standards such as WELL.

The fate of the City and the Office have become closely intertwined, one being the reason for the existence of the other. Modern cities flourish on the concentration of economic activity and population created by dense office districts, while downtown offices have come to depend on the ability of cities to agglomerate large talent pools as well as the urban and social infrastructure that enable these, often youthful, workforces to thrive.

Knee Jerk Reactions and the Right Lip Service

Now, one might wonder how much of this productivity plateau or spike, as the case may be, is because very few people would want to admit to being less efficient and effective at a time of global economic turmoil, with greater unemployment than at any time since the Great Depression. Likewise, unless the measurement of productivity fully captures the impact of the erosion of work-life separation and the greater hours that people may be putting in at home, longer but more fragmented work hours may be accounting for some of the purported positive effects. Clearly, there are likely many roles – especially those that are more process-oriented and which need less innovation or collaboration – where there might actually be comparable, if not enhanced, productivity. Likewise, the saving of time spent in the daily commute, especially in the world’s worst congested metropolises (think New York City, Bangalore or any number of others) is very real.

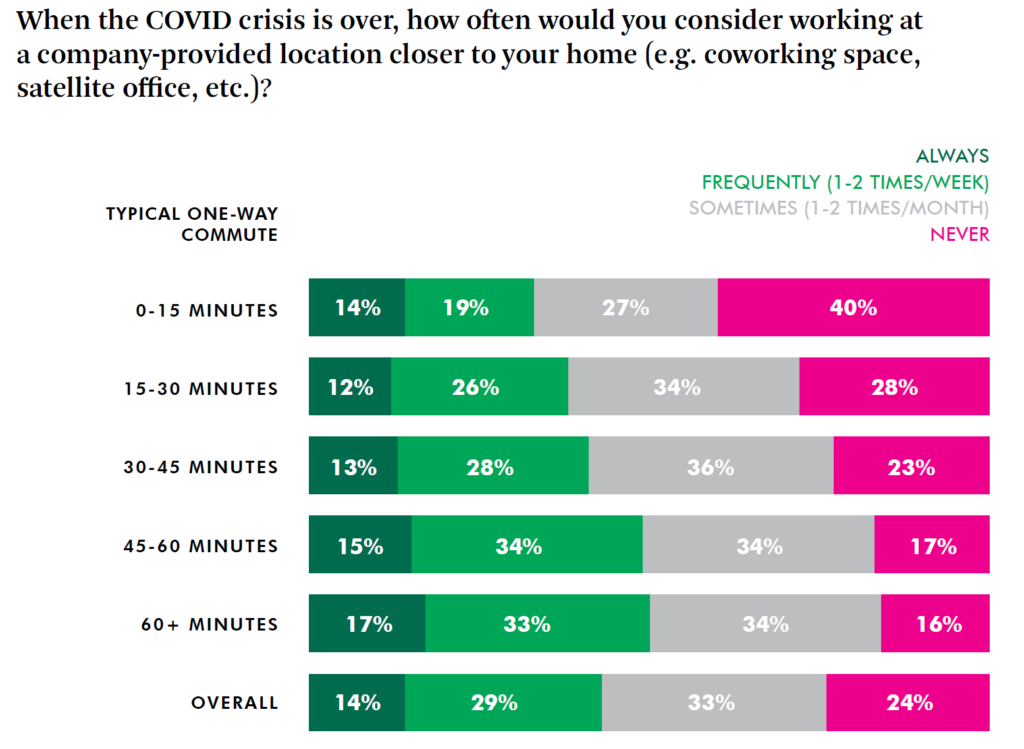

Not surprisingly, employees with long commute times are more likely to consider working from an option closer to or at their homes.

The Evidence for the Resilience of the Office

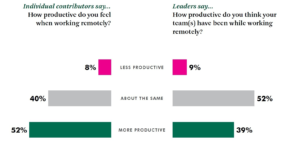

“In all candor, it’s not like being together physically. And so I can’t wait for everybody to be able to come back into the office. I don’t believe that we’ll return to the way we were because we’ve found that there are some things that actually work really well virtually. Tim Cook, CEO of Apple Inc” “Even in the Seattle region, where we have now sent a lot of people home, we’re realizing that some people would rather have workspace at work once the Covid-19 crisis goes away because they want dedicated workspace with good network connectivity. Satya Nadella, CEO on Microsoft Corp” “I don’t know the future better than anyone else. I think going back to work is a good thing. I think there are negatives to working from home…We’ve seen productivity drop in certain jobs and alienation go up in certain things. So we want to get back to work in a safe way.” Jamie Dimon, CEO of J.P. Morgan & Chase Co.You get the point, not everyone is a fan of going all-in on WFH. These are the influential leaders of some of the largest, most powerful employers on the planet and they can clearly see how the enforced absences as a consequence of the pandemic are impacting productivity and the overall performance of the organization. At the very least, not everyone is thinking of giving up all their offices and camping out in the living room forever. The broad majority of employers are also in favour of returning their workforce to the office with the option of working from home for a fraction of the time.

Source: Brookfield – The Future of the Office, August 2020

Before we put this down to a tyranny of the management, it has also become clear that the majority of employees also don’t want to be cooped up at home, bringing work home on a permanent basis.

Source: Brookfield – The Future of the Office, August 2020/Gensler WFH Survey, 2020

The Office is Still Essential

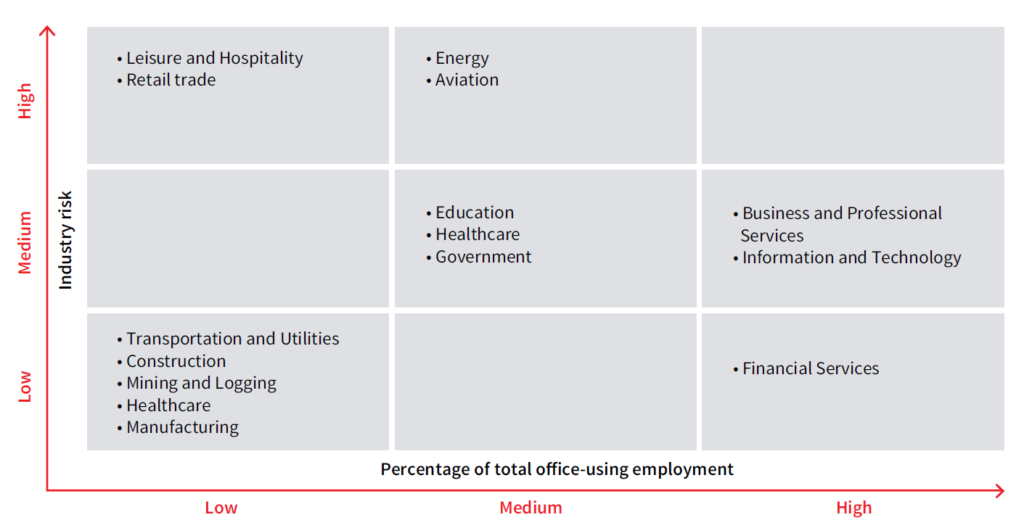

The Homo Sapien is a very social species, however unlikely it sometimes seems given how adept we are at in sowing divisions and fostering conflict. As society has switched from agrarian to knowledge-oriented industries, passing through industrial society along the way, the value of collaboration has snowballed. Work centred around the accumulation, assimilation and processing of various kinds of information, be it research and development of various kinds, financial services or consulting, has become the hallmark of developed societies and the tip of the spear for most economies, adding the most value per capita of employment. These are also the very industries that take up the bulk of office space around the world.

Source: JLL, Future of Office Demand, June 2020

The fact that these sorts of firms tend to like bringing their employees together in large, ever more collaborative offices and the phenomenon of the clustering of employers and employers into hub cities around the world, be it New York, Boston, San Francisco, Bangalore, London or Singapore, is primarily because of the what Professors Michael Porter and Paul Krugman posited as the principles of the development of business clusters/the economies of agglomeration. Putting smart people in physically proximate groupings has benefits for themselves and their organizations as it seems to accelerate the development of new ideas and concepts not only by facilitating greater formal collaboration but also through unstructured or even serendipitous interactions. Say, you run into your friend who works at another firm at the Starbucks near your offices and come up with a new idea over a venti-blonde-soy-latte-with-one-pump-of-hazelnut. Likewise, an abundant and diverse talent pool available in close proximity leads to multi-functional teams coming together in unstructured ways as well as in rapid acquisition of talent through informal channels such as word of mouth. Proximity to knowledge anchors, such as that of the East Cambridge life sciences and R&D cluster to MIT and Harvard University or Silicon Valley to Stanford University, is another key aspect of the clustering effects and here again, there are definite advantages to physical presence as opposed to being on the other side of the country or the world.

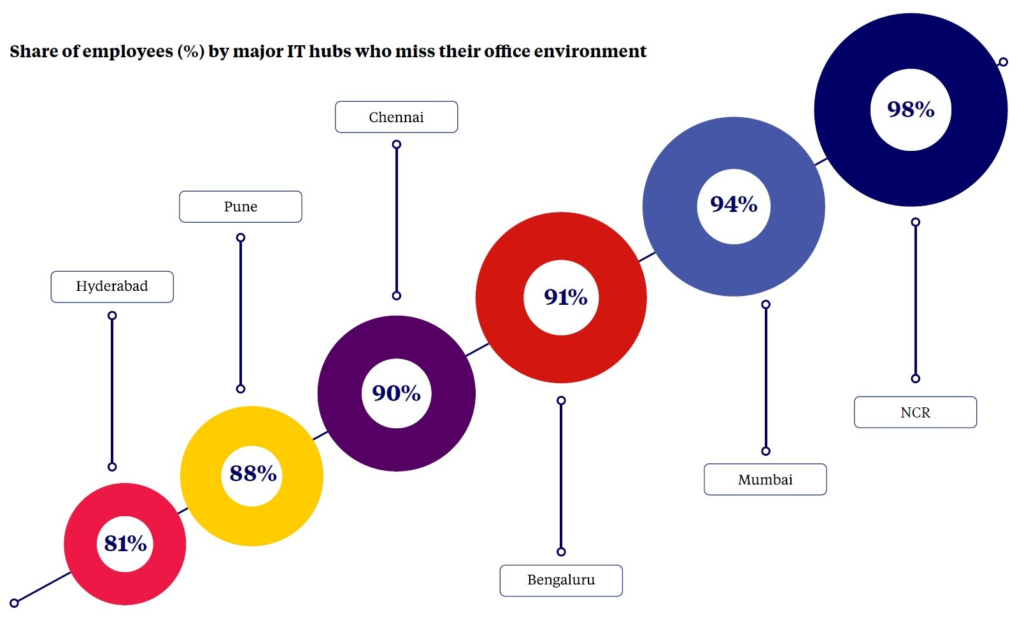

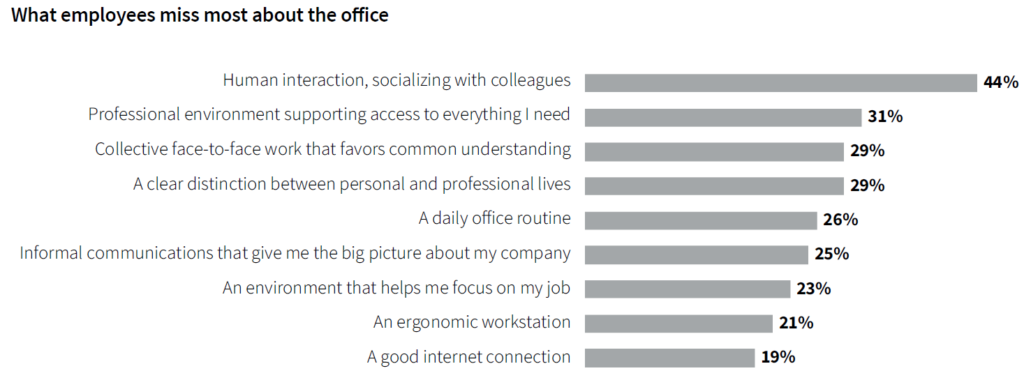

Beyond collaboration, employees have been missing the social aspects of being at the workplace including all the informal interactions with their colleagues (here’s looking at you, coffee machine and favourite dive after work, sigh!), the ability to mentor and be mentored and to stay in synch with the culture of the company. Offices also provide much more conducive work environments – better technology, workstations and amenities -and also help create a clearer division between work and life at home.

Source: JLL, Future of Office Demand, June 2020

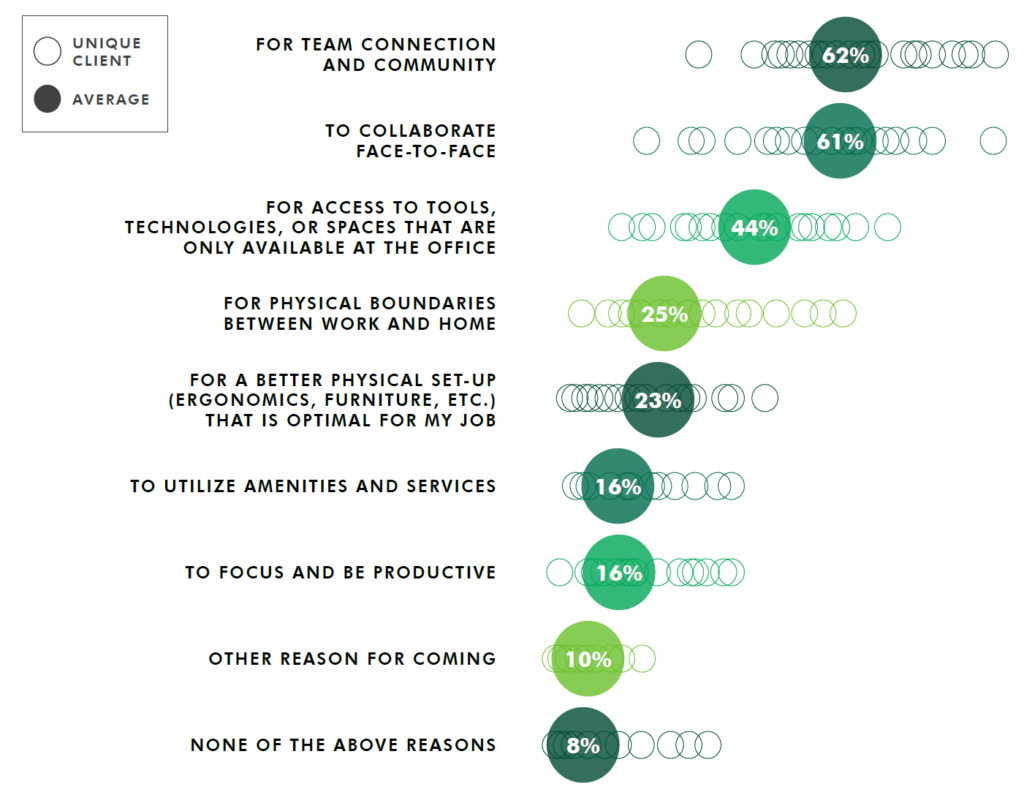

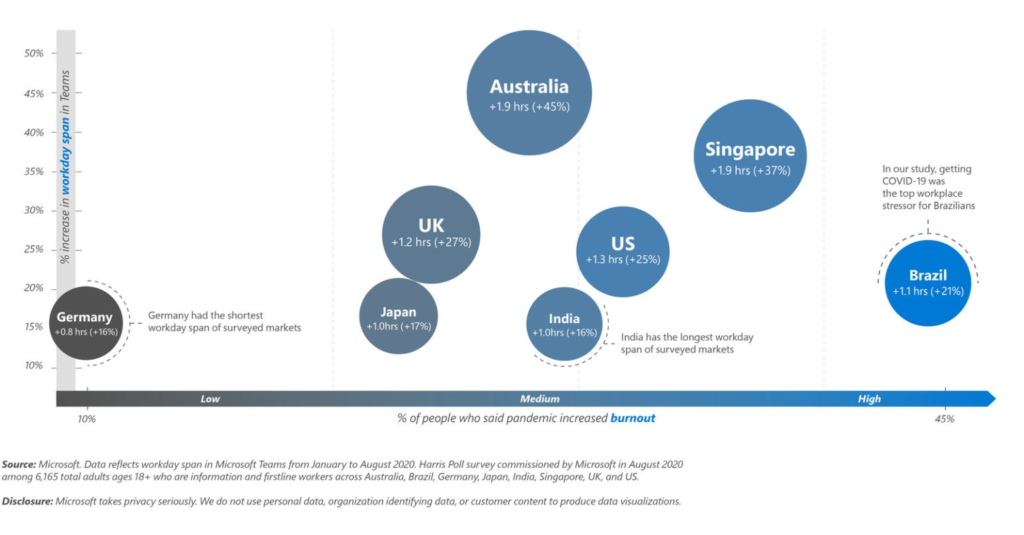

Coming from a firm that has greatly benefited from virtual collaboration and the shifting of work to the cloud (to the tune of many, many Billions in revenue and market capitalization), the research makes for very interesting reading. The lack of separation between work and life while working from home was cited as the top reason for increased levels of burn out, followed by the inability to interact with colleagues. This aligns with the studies quoted above and creates a clear picture of what we took for granted about the office that many of us used to lament going to day in and day out.

It even seems that the much-hated commute, often cited as yet another reason to never go back to the office, is an essential period of separation or transition between home and work, and vice-versa. The disappearance of the commute, long or short, has negatively impacted the separation between work and life, and enhanced burnout and eroded productivity.

“Commutes provide blocks of uninterrupted time for mentally transitioning to and from work, an important aspect of wellbeing and productivity. People will say, ‘I’m happy I don’t have to commute anymore. I’m saving time.’ But without a routine for ramping up for work and then winding down, we’re emotionally exhausted at the end of the day.”

– Shamsi Iqbal, principal researcher, Microsoft Research

Who would have ever thought that!

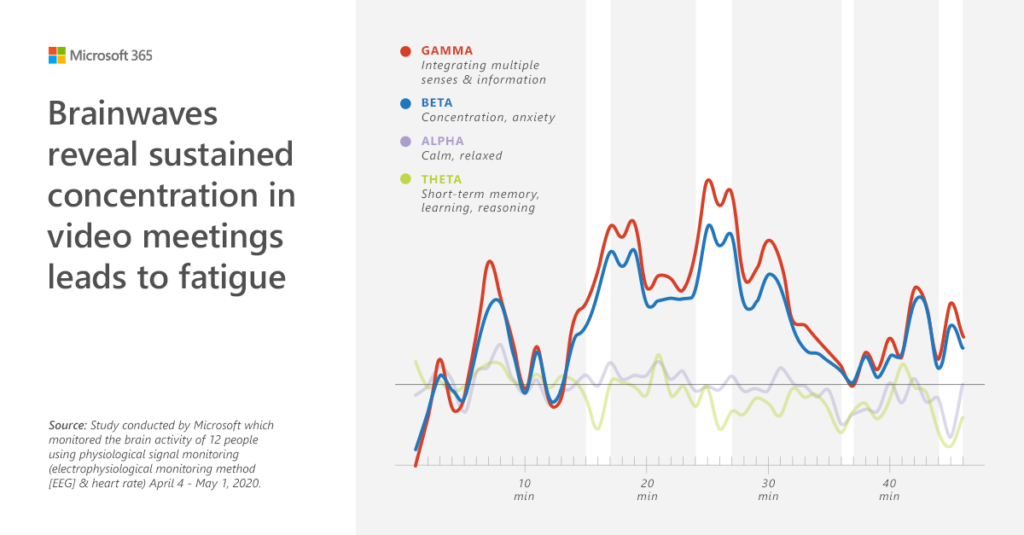

If you have been imagining yourself slowly, or not-so-slowly, slipping into insanity during those long virtual meetings that most of us find ourselves being inexorably drawn into these days, fear not, you are actually losing it! Researchers at Microsoft’s Human Factors Lab have been observing how the brainwaves of people participating in long virtual meetings undergo significant changes as they spend more and more time in front of the screen trying to make up a workable proxy for face-to-face time.

Adapting to the Post-COVID World

While it is evident that the office will not go extinct, not even close to it, we have to accept that the winds of change are blowing across the office landscape as tends to happen after any cataclysmic change in an ecosystem. Just like the pandemics and great fires of the past resulted in better sanitation and building standards, the impact of COVID-19 will necessitate changes in the physical nature of offices as well as in the way landlords approach their tenant relationships in order to ensure that tenants and their employees come back with a feeling of confidence in their workspaces and also continue to find value in occupying high-end office buildings around the world.

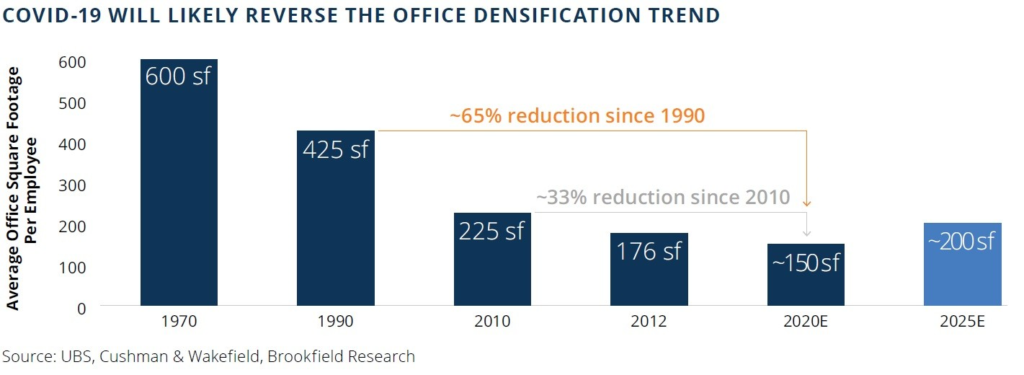

For example, years of densification at the office – squeezing more and more people into less and less space – are likely to reverse, both because of the need for distancing in the short and medium-term, and because of the office assuming a central role in collaboration, socialization and community building. Density is highest in Asian cities, with Indian cities like Bangalore and Mumbai having some of the smallest allocations, often as low as 75 Square Feet per person in open-plan, large floorplate, office buildings.

Source: Brookfield – The Future of the Office, August 2020

This trend may quite possibly not just negate the effects of the erosion in office demand due to the short and medium-term economic impact of the pandemic but may result in increased demand for space in the newest, best-designed office buildings. Of course, this implies that there will be an uneven distribution of pandemic-related impact on landlords, with some of the largest ones with the best located and highest quality portfolios doing better than others. On the flip side, owners of suburban offices may be benefited as firms look to diversify their footprint as opposed to consolidating all their offices in the largest cities.

1. Promoting Wellness through Technology

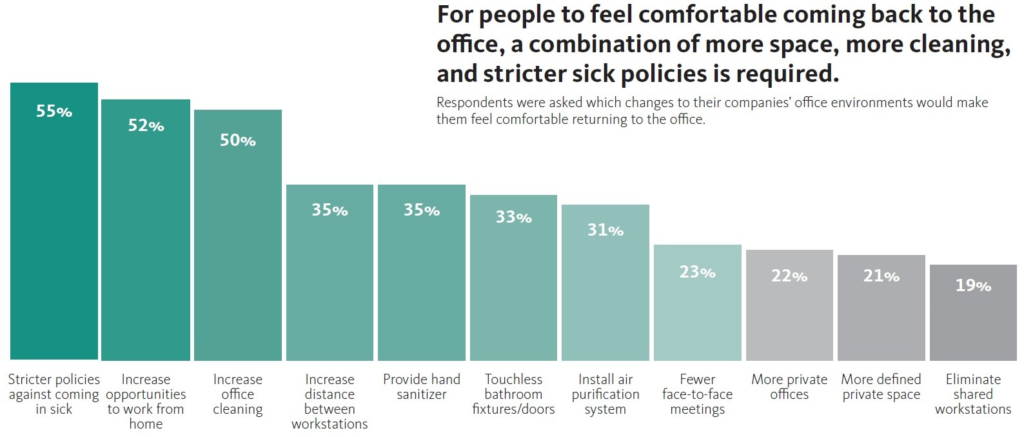

The pandemic has brought Health and Wellness to the fore in terms of priorities that tenants and their employees want landlords to address. Measures designed to enhance health and hygiene are not surprisingly high on the wish list for employees to consider returning to their offices.

Source: Gensler Work from Home Survey, August 2020

2. Changing Ways of Working

While 2020 will not spell the end of the office or the city, the events of the last nine months (yes, it has been THAT long since this started for those of us outside of China!) have accelerated many trends in the way we live, work and play. Just as the pandemic has expedited the growth of e-commerce and the switch to high quality, experiential, retail, offices too will see significant changes in how we work, many of these changes already have been underway well before the virus started doing the rounds.

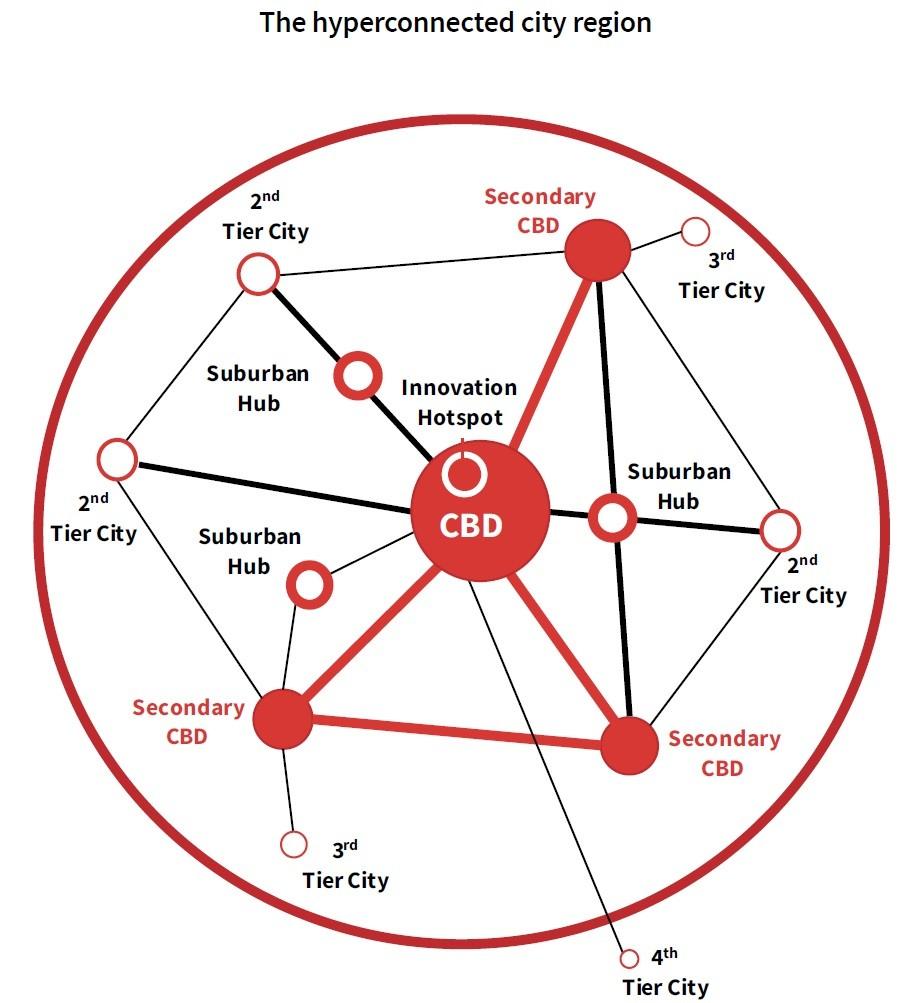

For example, there had already been an ever-increasing focus on the collaborative nature of work, as well as on enhancing innovation. The now-ubiquitous WFH had been present in some measure, although often with grudging acceptance by managers, in many organizations. Most, if not all, medium and large organizations were already used to working with teams distributed in multiple locations, often times on opposite sides of the planet. The accelerating growth of what are called Global In-house Centers (GICs) or Global Capability Centers (GCCs), which are in essence satellite offices of a company performing core activities such as R&D and trading, in India, Ireland and other countries is a clear indication that work is going where the talent is. In this sense, the validation that remote working can be made to work with at least a modicum of effectiveness in many industries also proves that work can be done as well by someone in Bangalore as in Bangor, Maine or in Trivandrum as in Tallahassee, Florida. This may, in turn, accelerate inter-country movements of roles as much or even more than intra-country transfers where employees head out from the big, expensive cities to smaller, less expensive places or even out to the pastoral idyll. JLL, for example, postulates a work ecosystem that encompasses various types of cities, ranging from the gateways to second and third-tier ones, over which a firm’s workforce may be distributed over the medium and long term.

Source: JLL Future of Office Demand report, 2020